Klarna is a Swedish company that provides financial services to e-commerce merchants and shoppers. The company’s “Buy Now Pay Later” model allows shoppers to finance their online purchases and pay for them over time. It also facilitates retail banking and offers shopping services that help consumers save money and time.

Since its founding in 2005, Klarna has grown to become one of Europe’s most valuable companies. It connects over 147 million consumers with more than 400,000 retailers globally and employs about 5,000 people. In FY 2021, the company recorded $80 billion in gross merchandise volume (GMV) and $1.6 billion in net operating income.

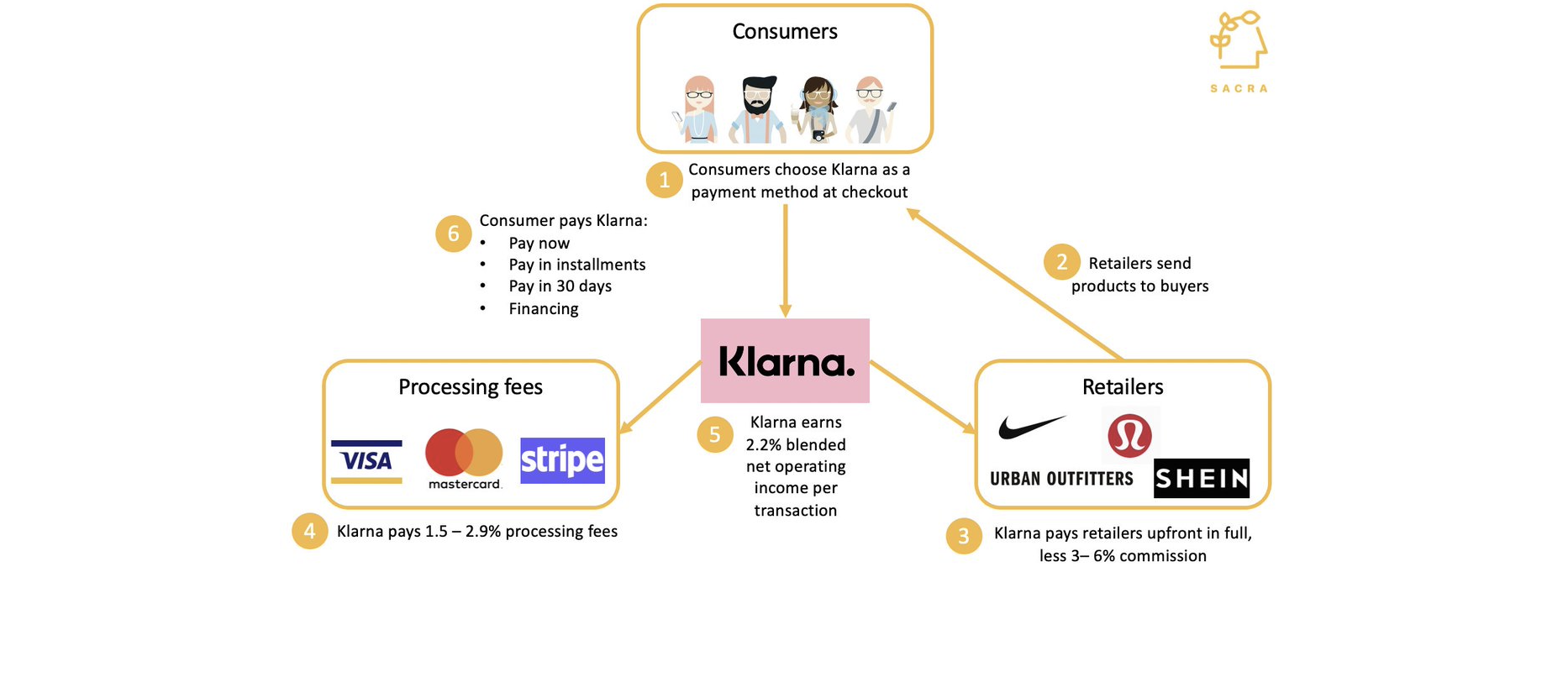

Klarna’s success lies in its unique business model, which allows it to generate revenue from multiple sources. Among these are merchant fees, interest income from consumer loans, interest on cash, and interchange fees. The company also earns revenue from other sources such as foreign exchange and late payment fees. Let’s find out more about how Klarna makes money.

Bottom Line Up Front

Klarna partners with e-commerce merchants to provide financing options to shoppers at the point of sale. The company charges merchants a fee for this service and interest on the loans it extends to shoppers. In addition, Klarna earns revenue from interchange fees, foreign exchange, and late payment fees.

Klarna’s Financial Overview

Klarna is a private company, so it doesn’t need to disclose its financials. However, the company has voluntarily published some financial data, which gives us an insight into its business model and revenue sources.

The company processes an estimated 2,000,000 transactions daily. The high transactional volume is a clear indicator that Klarna is a leading player in the industry. In FY 2021, Klarna’s GMV increased by 42% to $80 billion. During the same period, the company’s net operating income grew significantly, reaching $1.6 billion, up from $1.097 billion in FY 2020.

Despite impressive growth on the top line, Klarna’s bottom line has been facing some challenges. From 2013 to 2017, it reported increasing profits year on year. The company’s profitability took a hit in 2018, as profits dropped to $10.68 million (1105,224,000 Swedish Krona)

The drop in profitability stretched to progressing years, with a net loss of $91 million in 2019 and $140 million (1,375,809,000 Swedish Krona) in 2020. 2021 wasn’t any better, with a 337% YoY increase in net losses to $730 million. The company attributes its continued streak of losses to its expansion into new markets, credit defaults, and expansion of its BNPL product.

As of June 2021, Klarna had raised $3 billion in funding, thus raising its valuation to $46 billion. Through its unique underwriting, Klarna managed to reduce credit losses by 60% if we were to count as from 2019. It also saw triple growth in US volumes, with a 71% consumer increase to 25 million as of January 2022.

How Does Klarna Make Money?

Klarna prides itself as a growth partner and not just a lender to eCommerce merchants. The company doesn’t just lend money to merchants but also provides valuable insight into their business. AQs retailers look to establish consistency with their customer purchase cycle; they use Klarna to offer flexible payment options that match the retailer’s average order value and customer lifetime value.

The company generates revenue in four primary ways:

- Merchant Fees/Commissions

- Interest Charged on Consumer Loans

- Interest on Cash

- Late Fees

The company also makes money from other sources, such as foreign exchange, Klarna Card, and interchange fees.

Below is a breakdown of how Klarna makes money from the four main sources:

1. Merchant Fees/Commissions

Most of Klarna’s revenue comes from merchant fees. The company charges a commission on every transaction processed through its platform. The commission percentage of the total transaction value ranges from 3.29% to 5.99%, depending on the merchant’s country and payment method. It also charges a flat fee of $0.30 per transaction.

Klarna offers several payment methods, including Pay Now, which involves card payments, Pay in 30 days, and Financing, which offers 6,12,24, and 36-month terms. The company doesn’t charge any Setup Fee, Monthly Fee, or Minimum Volume Commitment from the merchants.

It also provides an Instant Shopping Solution, a service that allows customers to check out faster, whether onsite or offsite. Klarna charges a variable fee of 3.29% onsite and 3.79% offsite from the merchants for this service. The instant shopping solution guarantees a fluid shopping experience that helps boost sales and conversion rates for merchants.

See also: How Does GoodRX Make Money

2. Interest Charged on Consumer Loans

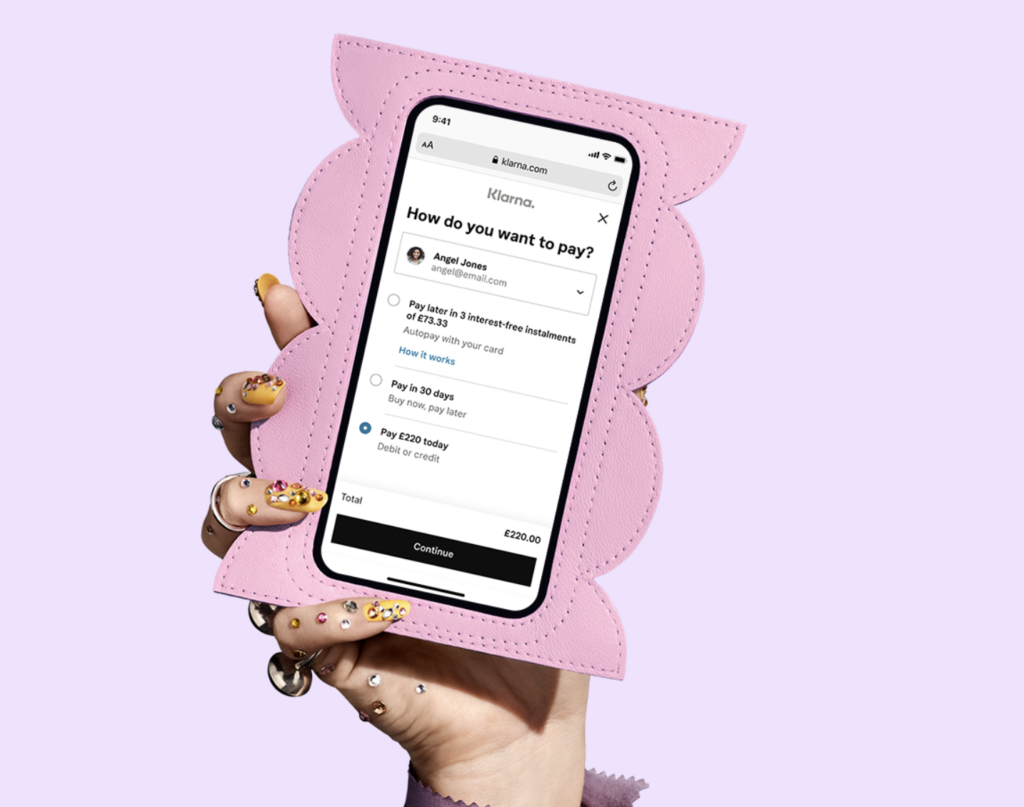

Klarna is a financial services provider, and, as such, it also charges interest on the loans it provides to consumers. Its financing products allow consumers to spread the cost of their purchase over time.

Apart from the fee and flat rate, the company also charges an Annual Percentage Rate (APR) of 0% to 19.99% on all financing products. The APR is the cost of borrowing, expressed as a yearly rate. It includes the interest rate, loan fees, and other charges.

3. Interest on Cash

Klarna is also a banking company, and, as such, it uses the money residing in customer accounts to invest in different financial instruments to generate returns. The company invests exclusively in high credit quality sovereign government-rated securities with short maturities.

This strategy provides stability and security to the money in customer accounts while generating returns that contribute to Klarna’s profits. However, it’s not 100% safe as any exposure to credit risk, market risk, or liquidity risk could result in losses.

Governments and municipalities have the potential to expose Klarna to credit risk through repurchase agreements, collateralized debt obligations, and commercial paper programs. Klarna invests only in rated securities to mitigate such risks and diversifies its investments across different issuers and industries.

It also offers traditional loan options to business customers, and the company earns an Annual Percentage Rate (APR) of 0% to 24.99%. The loans have terms ranging from 3 to 36 months, and there’s no origination fee. However, this service is only available at select retail stores.

4. Late Fees

If customers fail to pay before the order invoice due date, they’re charged a late fee. However, Klarna has caps on late fees, which means customers will be charged per late payment and not the total outstanding balance. Moreover, if the total order value doesn’t exceed $49.99, the late fee per installment doesn’t count. However, if the order value is more than $50, the late fee equals $3 per installment and $9 across the three late installments.

Klarna charges late fees to encourage customers to make payments on time and to offset the cost of collections. All unpaid debts and missed payments go to debt collection agencies, further damaging the customer’s credit score. It’s impossible to change the due date of a financing plan, but customers have the option of extending their payment due date.

See also: Meg Whitman Bio: How Did She Become One of the Richest Women on Earth?

5. Interchange Fees

Card-issuing banks charge interchange fees to the merchant’s bank for processing card payments. The fees are a percentage of the total transaction value and vary depending on the card type, country, and merchant type. With the 2021 launch of Klarna bank accounts for the German market, the company will be able to collect these fees.

In 2021, the company unveiled UK and US credit cards that generate interchange fees. The Klarna credit card allows customers to shop anywhere and earn rewards in cashback and Klarna points. Users can save with the bank, set goals, and manage their money in one app.

Anytime a user pays with a debit or credit card, the merchant pays an interchange fee to the card issuer. The fee is generally less than 1% for debit and credit cards. Klarna receives a cut of this fee, which is how the company makes money from credit and debit card payments.

Klarna’s Business Model and Strategy

Klarna’s focus on expanding into new markets and product categories has helped the company grow fast. Through partnerships with retailers, the company has offered its financing products to millions of consumers. Klarna partners with more than 250,000 retailers globally, including big names such as Macy’s, H&M, IKEA, and Nike.

These partnerships are important for two reasons. First, they help Klarna generate revenue from fees charged to retailers. Second, they help the company acquire new customers. Klarna’s emphasis on building brand equity has also helped the company differentiate itself from its competitors. The company creates emotional relationships with its customers through marketing campaigns that focus on personal stories.

In May 2022, Klarna CEO Sebastian Siemiatkowski said that the company planned to focus on short-term profitability rather than growth. The company had been loss-making since 2019, but plowing money into expansion. He also announced that they’ll continue doing business as a private company and won’t pursue an initial public offering (IPO) soon.

The company’s long-term goal is to disrupt the retail payments and banking industry. It wants to become the go-to financial services provider for all things related to shopping. Klarna needs to continue expanding its product offerings and geographical reach.

However, with that comes the risk of growing too quickly and not being able to sustain profitability. The company has to change its path toward its primary goal to focus on short-term profitability as they work toward the long-term goal.

Klarna’s Risk Management and Loss Mitigation Strategy

To achieve profitability, any company needs to have a solid risk management strategy. Given the economic conditions of the past decade, this has become even more important. Klarna uses a three-line defense model where the first line of defense is to own the risk and perform necessary controls to secure acceptable risk exposure.

The second line of defense is the risk control, compliance, and engineering assurance functions. This line established policies that facilitate risk assessment and provides tools for monitoring and managing risks. The third and final line of defense is the internal audit function, which provides an independent evaluation of the risk management framework.

Klarna has taken several measures to mitigate the risks associated with its business model. First, the company has established a robust risk management framework. This helps to identify, assess, and proactively manage risks. Second, Klarna has built a diversified business model that generates revenue from multiple sources. This reduces the impact of any one risk on the company’s overall performance.

Third, Klarna has a strong focus on customer satisfaction. This helps to reduce the likelihood of customers defaulting on their payments. Finally, Klarna has built a good reputation in the industry, thus protecting it from reputation risk.

Klarna’s Credit Risks

Despite these measures, there are still some risks associated with Klarna’s business model. The most significant is the credit risk associated with its financing products. Even if Klarna were to make all of its loans on a non-recourse basis, the company would still be exposed to the risk of customer defaults.

Essentially, it provides unsecured loans to consumers who may not be able to repay them. To mitigate this risk, Klarna uses several methods. One of these methods is proprietary scoring methodologies. By performing credit assessments on its customers, Klarna can identify those likely to default on their payments.

Another method is proactive tracking and controlling merchant risk. Klarna monitors the behavior of merchants who offer its financing products to their customers. The company can implement longer payment terms or withhold payments to merchants who exhibit high levels of risk.

Another method is selecting high-quality counterparties and setting exposure limits. Klarna carefully selects the financial institutions it does business with. It also limits its exposure to any counterparty by entering into multiple contracts with different counterparties.

Finally, Klarna maintains a diversified funding mix. The company funds its operations through a mix of equity, debt, and commercial paper. This diversification reduces the impact of any one funding source on the company’s overall performance.

FAQs

Question: What is the downside of Klarna?

Answer: Before customers can use Klarna to finance their purchases, they must first provide their personal information and agree to a credit check. While it’s necessary to do a credit check, some customers may find it off-putting. Moreover, those who fail the credit check cannot use Klarna may be an inconvenience.

Question: Does Klarna impact your credit score?

Answer: Klarna may affect your credit score in a few ways. Your credit score will drop if you make late payments or miss payments altogether. However, it also does soft checks when you first sign up for an account, which doesn’t have an impact on your score. The most significant factor is whether or not you pay off your Klarna balance in full and on time each month.

Question: Why Is Klarna so successful?

Answer: Klarna is successful for a few reasons. First, it’s very convenient for customers. They can finance their purchases and spread the cost over time without worrying about interest or fees.

Second, it’s straightforward to use. Customers can sign up for an account and start using Klarna with a few clicks. Finally, Klarna is very popular with retailers. It’s partnered with over 200,000 stores worldwide, so customers have plenty of options when it comes to where they can use Klarna.

Conclusion

Klarna is a financial services company that offers financing products to consumers and businesses. The company makes money by charging interests in traditional loans, interest on cash, interchange fees, and merchant fees.

Klarna has a strong focus on customer satisfaction and credit risk management, which has helped it become one of the world’s most successful financial technology companies. It’s currently partnered with over 200,000 stores in 17 countries and is available to customers in most parts of the European Union.

Recommended Reads:

- Gary Vaynerchuk Bio: From Wine Lover to Millionaire

- Carvana Competitors Analysis

- GameStop Competitors Analysis – Top 9 Competitors

- Matterport Competitors Analysis

- ADP Competitors Analysis: Is Their Market Position Stable?

- How Does Honey Make Money : Is It Safe?

- Dan Bilzerian Bio - December 9, 2022

- OLA Model Explained - November 23, 2022

- Service Value Chain Explained - November 23, 2022